Condition ratings drive everything in an appraisal - from value adjustments to lender decisions to outright deal-killers. Yet most firms still rely on vague descriptors like "average" or "good" that mean completely different things to different appraisers, reviewers, and underwriters.

The gap between what an appraiser sees in the field and what ends up in the report creates real operational headaches. One appraiser's C3 is another's C4. Photos don't match descriptions. Underwriters challenge ratings. Revision requests stack up. Everyone wastes time arguing over subjective calls instead of moving deals forward.

What works is anchoring each condition rating to specific photo requirements, exact phrasing templates, and clear escalation triggers. Not general guidelines - precise operational standards that close the interpretation gap between field inspection and final report.

The real cost of inconsistent condition ratings

Appraisal firms lose money on condition rating problems in three ways that compound over time.

First, the revision spiral. When underwriters challenge a condition rating, the appraiser has to dig through photos, justify the call, potentially revise the report, and resubmit. Each revision runs somewhere in the $45-85 range in staff time. Firms handling 400+ appraisals monthly see roughly 15-20% challenged on condition ratings alone - that's anywhere from $3,600 to $6,800 monthly in pure rework cost, depending on volume.

Second, the training tax. New appraisers take months to calibrate their condition assessments to firm standards because those standards usually live in someone's head rather than a documented rubric. Senior appraisers end up spending 3-5 hours a week reviewing and correcting condition calls. At $75/hour, that's $15,000+ annually per senior appraiser doing quality control instead of revenue work.

Third, reputation damage. Lenders track revision rates by firm. High revision rates on condition ratings signal poor quality control. Once a firm gets labeled "requires extra review," every appraisal gets scrutinized harder, which creates more revisions in a downward spiral. Some firms lose preferred vendor status entirely over consistency problems.

The root issue isn't appraiser judgment - it's the absence of clear, photo-anchored standards that produce consistent outputs regardless of who does the inspection.

Building your five-point condition framework

Most appraisal firms default to Fannie Mae's C1-C6 ratings without adapting them to operational reality. The descriptions are too broad. Photo requirements too vague. Escalation points undefined.

Manage every appraisal with confidence and clarity.

Rateoly helps you coordinate inspections, generate reports, and communicate seamlessly with clients.

- Comprehensive appraisal tracking

- Automated client notifications

- Integrated scheduling & report management

No credit card required

A working condition rubric needs three components that actually work together:

-

Required photo angles by rating level. Not "take exterior photos" but "front elevation showing roof line, all visible windows, foundation interface, and any exterior mechanical equipment." Each condition level requires specific shots that prove the rating.

-

Exact phrasing templates. Not "describe the condition" but pre-written phrases that match photo evidence. C3 kitchen: "Cabinetry shows normal wear consistent with age, hardware functional, countertops exhibit minor surface scratches not affecting utility." Remove interpretation. Standardize the language.

-

Escalation triggers. Clear rules for when to bump a rating. "If any two major systems (HVAC, roof, plumbing, electrical) show deferred maintenance indicators, minimum rating is C4." No debate. The evidence drives the rating.

Here's what this looks like operationally:

C1/C2 - New or Like New Construction

Required photos:

-

All four exterior elevations showing zero weathering

-

Interior room-by-room including ceilings and floors

-

Close-ups of all fixtures, hardware, and finishes

-

Mechanical systems with visible model/serial numbers

-

Attic and crawl space if accessible

Standard phrasing:

"Property exhibits no visible wear, deterioration, or deferred maintenance. All building components appear new or recently installed within 24 months. Finishes remain in original condition without evidence of use."

Escalation trigger:

Any visible wear pattern, settlement crack over hairline width, or evidence of occupancy automatically moves to C3.

C3 - Well Maintained with Normal Wear

Required photos:

-

Front and rear elevations showing overall condition

-

Kitchen showing cabinetry, appliances, and countertops

-

Primary bathroom fixtures and finishes

-

Flooring transitions and high-traffic areas

-

One photo demonstrating typical wear (scuff marks, minor scratches)

Standard phrasing:

"Property shows normal wear consistent with age and typical occupancy. All major components remain fully functional. Minor cosmetic imperfections present but do not affect marketability or utility. Deferred maintenance limited to routine items."

Escalation trigger:

Evidence of water stains, non-functioning major appliances, or deferred maintenance on any major system moves to C4.

C4 - Some Deferred Maintenance

Required photos:

-

Specific areas showing deferred maintenance

-

Wide shots providing context for maintenance items

-

Close-ups of deficiencies (peeling paint, worn flooring, damaged fixtures)

-

Exterior shots showing roof, siding, or window conditions

-

Any safety-related concerns

Standard phrasing:

"Property exhibits deferred maintenance affecting [specific systems/areas]. Required repairs include [list specific items]. Property remains habitable but shows obvious signs of delayed upkeep. Some functional obsolescence may be present."

Escalation trigger:

Any structural concern, evidence of active water intrusion, or non-functioning major system (heating/cooling/plumbing) moves to C5.

C5 - Obvious Deferred Maintenance

Required photos:

-

All areas of significant deterioration

-

Structural concerns if visible

-

Non-functioning systems or components

-

Safety hazards clearly documented

-

Overall context shots showing property condition

Standard phrasing:

"Property requires immediate repairs to [list major systems]. Significant deferred maintenance affects habitability/marketability. Repairs needed include but not limited to [specific list]. Property may not qualify for traditional financing without repairs."

Escalation trigger:

Structural damage, foundation issues, or conditions making the property uninhabitable move to C6.

C6 - Substantial Damage

Required photos:

-

All damaged areas from multiple angles

-

Structural problems clearly visible

-

Context shots showing extent of damage

-

Safety hazards prominently featured

-

Wide shots demonstrating overall deterioration

Standard phrasing:

"Property exhibits substantial damage requiring extensive repairs to achieve habitability. Major structural/system deficiencies present including [specific list]. Cost to cure likely exceeds 40% of as-repaired value. Property suitable for cash transactions only."

Escalation trigger:

Structural damage, foundation issues, or conditions making the property uninhabitable move to C6.

Photo requirements that support defensible ratings

Generic photo requirements create revision requests. "Take pictures of deficiencies" means nothing operationally. Every photo needs a purpose tied directly to the condition rating.

The field photo standards that pass lender review covered technical requirements. Here we're mapping specific shots to condition evidence.

For C3 properties, you need comparison context. A photo showing minor wear needs an adjacent area showing no wear - this proves the wear is isolated, not pervasive. A scratched hardwood floor photo should include a section of undamaged flooring in the same frame.

For C4 properties, document both the deficiency and its extent. A water stain photo needs a wide shot showing what percentage of the ceiling is affected. A damaged cabinet photo needs context showing whether it's one door or the entire bank.

For C5 and C6 properties, safety documentation becomes critical. Every potential hazard needs multiple angles. Exposed wiring gets a close-up plus a room shot showing location. Structural cracks get measured with a ruler in frame plus overall wall coverage.

The rubric should specify minimum photo counts by rating:

| Condition Rating | Minimum Photos | Key Documentation Focus |

|---|---|---|

| C1/C2 | 25 | Full coverage of all spaces |

| C3 | 20 | 3-5 showing typical wear |

| C4 | 25 | 8-10 documenting deficiencies |

| C5 | 30 | 15+ showing required repairs |

| C6 | 35 | Comprehensive damage documentation |

These aren't arbitrary numbers. They reflect what it actually takes to build a defensible file at each condition level.

Exact phrasing that eliminates interpretation

Vague descriptions kill credibility. "Kitchen in average condition" tells the reader nothing. "Some updating needed" invites interpretation debates. The condition rubric needs precise language templates that match photo evidence.

Build a phrase library for each condition level and component:

Flooring phrases by condition:

-

C3

"Hardwood floors show typical traffic patterns in main pathways, finish intact, no structural concerns"

-

C4

"Carpet exhibits wear patterns exceeding normal use, stretching evident in high traffic areas, replacement recommended within 12-24 months"

-

C5

"Flooring substrates visible through worn surfaces, transitions damaged creating trip hazards, immediate replacement required"

Kitchen phrases by condition:

-

C3

"Cabinetry doors and drawers operate properly, minor finish wear on high-use areas, countertops show light scratching consistent with normal use"

-

C4

"Several cabinet doors misaligned, drawer slides failing on roughly 30% of drawers, countertop burns/deep scratches present, appliances near end of useful life"

-

C5

"Cabinet boxes show water damage, multiple doors missing or non-functional, countertops delaminating, appliances non-operational"

Roof phrases by condition:

-

C3

"Shingles show normal weathering for age, no missing/damaged sections visible, gutters clear and properly attached"

-

C4

"Scattered lifted shingles visible, granular loss evident in multiple areas, gutters show rust/separation at several joints"

-

C5

"Multiple shingles missing, exposed underlayment visible, active leaking evident by interior stains, complete replacement required"

These aren't suggestions - they're copy-paste templates that keep language consistent across all appraisers. The photo evidence determines which phrase applies.

Escalation triggers that remove judgment calls

Most operational friction comes from borderline cases. Is that water stain enough to trigger C4? Does that foundation crack warrant C5? Clear escalation rules remove the debate entirely.

Automatic C4 triggers:

-

Any water stain over 2 square feet

-

Non-functioning major appliance

-

Carpet requiring replacement within 24 months

-

Exterior paint failure on 20%+ of any elevation

-

Missing or damaged flooring covering 10+ square feet

Automatic C5 triggers:

-

Any structural movement/damage visible

-

Heating or cooling system non-functional

-

Evidence of active water intrusion

-

Electrical hazards present (exposed wiring, damaged panels)

-

Plumbing leaks affecting habitability

Automatic C6 triggers:

-

Foundation failure evident

-

Structural members compromised

-

Fire/flood damage affecting 30%+ of property

-

Mold contamination requiring professional remediation

-

Property deemed unsafe for occupancy

These triggers work like a checklist during photo review. See a trigger condition? The rating moves up. No discussion needed. The compliance and evidence framework helps track when triggers override initial field assessments.

Operationalizing the rubric across your team

Creating the rubric is step one. Making it stick requires something more systematic.

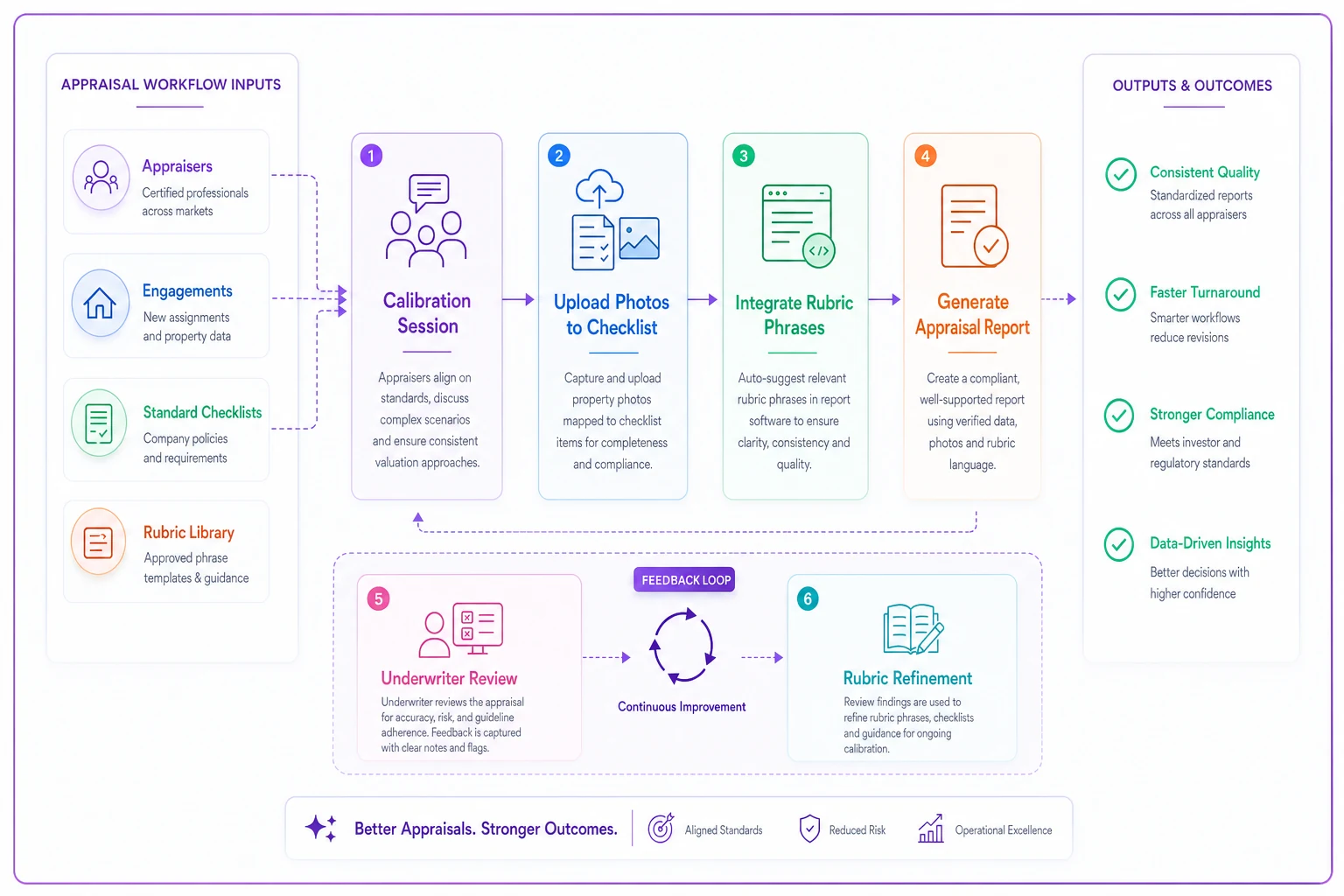

Start with a calibration session using real photos from recent appraisals. Pull 20 properties your team has completed. Have each appraiser independently rate them using the new rubric. Compare results. Where ratings differ, figure out which trigger or photo requirement wasn't clear enough. Refine based on those gaps.

Build the rubric directly into your workflow - not as a separate document appraisers have to remember to reference. Embed photo requirements in the inspection checklist. Add phrase templates to your report writing software. Create dropdown menus with the exact language options.

This illustration shows the calibration-to-embedding workflow in one view.

Embed photo requirements directly in the inspection checklist to reduce dependence on memory during fieldwork.

Track deviation patterns. When an underwriter challenges a condition rating, document whether the rubric was followed. If yes, the rubric needs adjustment. If no, the appraiser needs coaching. That feedback loop continuously improves the system.

Most firms see revision rates on condition issues drop significantly within 90 days of implementing a photo-anchored rubric. Not because appraisers suddenly got better at judging condition, but because the system removed judgment from the equation.

Special situations and property types

Historic properties: Age-related wear can't trigger the same downgrades. Original materials in good condition might show more wear than modern materials but represent higher value. Add a parallel track - "CH3" for historic properties with character-appropriate wear.

Luxury properties: High-end finishes change the baseline. Granite with minor chips might be C3 in a standard home but C4 in a luxury context where perfection is expected. Create finish-grade modifiers for your standard ratings.

Rural properties: Outbuildings, wells, and septic systems need their own rating criteria. A house might be C3 while the barn is C5. Document each structure separately with its own photo set and rating.

Mixed-use properties: Residential portions might rate differently than commercial spaces. A live/work loft could have a C3 living space with a C4 commercial kitchen. Split the ratings and photo requirements by use type.

Standard residential properties are straightforward. Special situations need rubric modifications.

Turning the rubric into competitive advantage

Firms with documented condition rubrics tend to see three operational improvements beyond fewer revisions.

Training accelerates significantly. New appraisers reach consistency in weeks instead of months because the rubric removes the fuzzy "learning period" where their work needs heavy review. They follow the photo requirements, apply the triggers, use the standard phrases - and their first reports match senior appraiser quality on condition assessments.

Client confidence increases. Lenders notice when a firm's condition ratings are consistent and defensible. Some firms share their rubric directly with lender partners, essentially saying "here's exactly how we determine ratings." That transparency builds trust and often leads to preferred vendor relationships.

Technology adoption becomes easier too. When you have clear, documented rules for condition assessment, you can start automating parts of the process. AI-powered operational software can pre-screen photos against your requirements, flag missing shots, and suggest appropriate ratings based on visible evidence. The rubric becomes the foundation for smarter workflows - but only if the rubric itself is solid.

The manual photo review process - comparing images against mental standards, debating appropriate ratings, crafting unique descriptions from scratch - consumes 20-30 minutes per appraisal in most firms. A well-designed rubric cuts that to under 10 minutes. With the right software supporting it, you're looking at a few minutes of verification rather than creation.

Making the rubric stick

The best rubric fails if appraisers don't use it consistently. Adoption requires both incentives and accountability.

Make compliance visible. Track rubric usage by appraiser and share weekly metrics showing who's following the system. Celebrate consistency. Call out improvements where they happen.

Connect rubric use to compensation. Some firms add a quality bonus for appraisers with zero condition-related revisions over a quarter. Others adjust pay for revisions caused by not following the rubric. Either approach makes the standards real in a way that policy memos don't.

Update quarterly based on actual patterns. If certain triggers keep getting challenged by underwriters, refine them. If specific photo angles keep getting requested in revisions, add them to requirements. The rubric should evolve based on real operational friction, not theoretical standards set once and forgotten.

Build it into your tech stack. Whether using off-the-shelf appraisal software or custom solutions, the rubric should be embedded in the tools. Photo upload screens should show required angles. Report sections should offer phrase dropdowns. Triggers should surface automatically based on uploaded images.

Beyond individual appraisals

A photo-anchored condition rubric does more than standardize individual reports. It creates operational intelligence across your entire portfolio.

Track condition trends by geography. If one ZIP code consistently shows C4/C5 ratings while adjacent areas are C3, you've identified a declining market before MLS data reflects it. That intelligence helps with comp selection and adjustment decisions.

Identify inspector blind spots. If one appraiser's C3 ratings get challenged more than others, their photo angles might be missing key evidence. The rubric helps diagnose whether it's a photography problem or a judgment problem.

Flag revision risks before submission. When a report has borderline triggers - just under the threshold for escalation - catch it internally before it goes out. Edge cases reviewed in-house don't become external challenges.

The rubric essentially becomes a real-time quality control system. Each photo upload, each condition selection, each phrase choice either follows the system or triggers review. Quality management shifts from reactive to preventive.

The path forward

Most appraisal firms know their condition ratings need work. The revision requests, the inconsistent reports, the training struggles - these symptoms all point to the same root cause: no systematic standards.

-

Pull five recent C3 properties from your completed files

-

Document the photos that prove each rating

-

Write exact phrases for each property component

-

Define the triggers that would have moved each to C4

-

Test the draft rubric with your team using real properties

-

Refine wherever disagreements surface

-

Embed the final version into your existing workflow tools

Start with your five most recent C3 properties. Document exactly what photos prove that rating. Write the exact phrases that describe that condition. Define what would have pushed them to C4. Build from real examples, not theoretical frameworks.

The firms winning on efficiency aren't always the ones with the best appraisers. They're the ones with the best systems. A photo-anchored condition rubric is one of those systems that pays back quickly - fewer revisions, faster training, cleaner communication with clients.

In an industry where subjective judgment creates objective problems, operational standards are the fix. Not more training on how to judge condition, but clear rules that remove judgment from the equation entirely. The question isn't whether you need a condition rubric - it's whether you build one proactively or keep absorbing the cost of inconsistency in revisions, rework, and lost client confidence.

Ready to elevate your appraisal operations?

Join 500+ appraisal firms using Rateoly to enhance accuracy, save time, and improve client satisfaction.