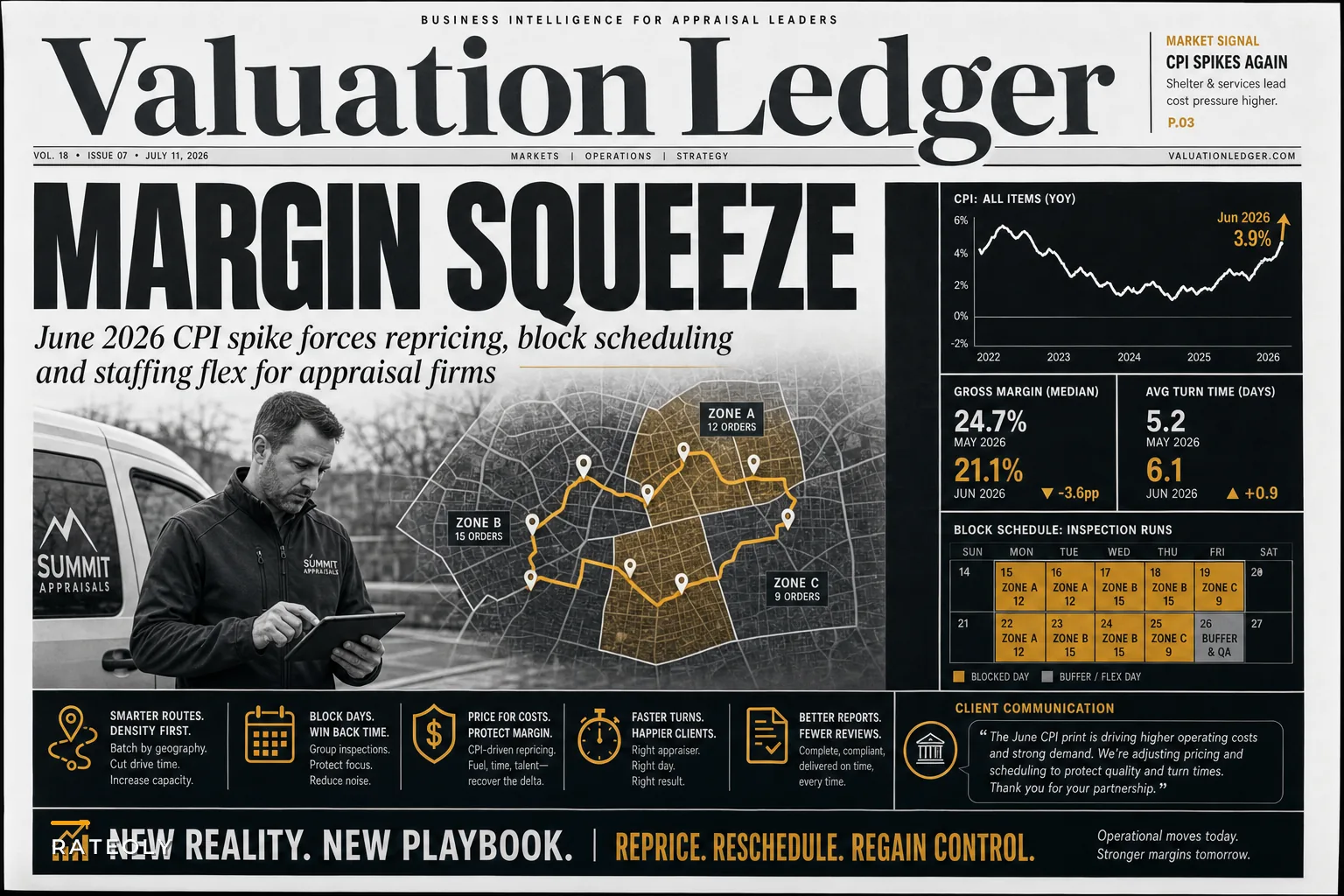

The Bureau of Labor Statistics dropped their June 2026 CPI data yesterday morning, and while headline inflation looks controlled, the shelter and services components tell a different story for appraisal operations. Shelter costs jumped 0.4% month-over-month—annualized that's close to 5%—while core services inflation keeps running hot at 4.8% year-over-year.

For appraisal firms, this creates an immediate operational problem. Input costs are climbing (fuel, insurance, contractor labor) while mortgage rates will likely tick up another 25-50 basis points by August, cutting into refinance demand. Firms are already seeing order volumes drop 15-20% from May peaks, but their cost base hasn't adjusted to match.

This isn't a macroeconomics discussion. It's about next week's scheduling board and next month's P&L.

The hidden cost spiral most firms miss until Q3

Every appraisal shop tracks revenue per order. Almost none track true cost per inspection mile. When gas prices bump up $0.40 per gallon and your appraisers are driving 140 miles daily across scattered assignments, that's roughly $11 extra per day per appraiser. Add commercial auto insurance adjustments—up around 8% YTD in most states—and suddenly your margin on a standard residential appraisal quietly dropped $35-40 without anyone flagging it.

The real damage happens when firms try to maintain service levels with the old cost structure. You keep accepting rush orders at standard fees. You send appraisers on single-property trips to protect 48-hour turn times. You absorb higher costs assuming volume bounces back in Q3.

What actually tends to happen: margins compress from around 28% down to 19% over two quarters. Cash gets tight. You delay software upgrades, skip the fall conference, maybe lose your best admin. Service quality slips. Lenders notice. Orders start flowing to competitors who adjusted in July instead of waiting until October.

Where traditional pricing models break down

Most firms still price by property type and turnaround time.

Manage every appraisal with confidence and clarity.

Rateoly helps you coordinate inspections, generate reports, and communicate seamlessly with clients.

- Comprehensive appraisal tracking

- Automated client notifications

- Integrated scheduling & report management

No credit card required

| Type | Price |

|---|---|

| Residential | $450 |

| Rush | add $125 |

| Complex property | $650 |

That worked when gas was $2.80 and appraisers could realistically hit 4-5 inspections a day.

June 2026 CPI data shows transportation costs up 6.2% year-over-year. Your field costs just increased roughly $2,800 per appraiser annually, and pricing hasn't moved. On top of that, the geographic spread of orders has widened as suburban and exurban purchases dominate the mix. That "standard" $450 residential order might now require 55 miles of driving versus 30 miles two years ago.

The firms surviving this squeeze have moved toward cost-based dynamic pricing. They track actual drive time, complexity scores, and seasonal demand patterns. A 35-mile rural inspection gets priced at $485. An 8-mile suburban tract home stays at $425. Rush orders during peak weeks add $175, not $125.

One regional firm in the Midwest rebuilt their pricing matrix last month. They analyzed around 1,100 completed orders from Q1, mapping actual costs including drive time, report complexity, and revision rounds. They found 31% of their orders were priced below breakeven once real costs were allocated. After implementing tiered geographic pricing and complexity multipliers, gross margin improved 4.2 percentage points in about three weeks.

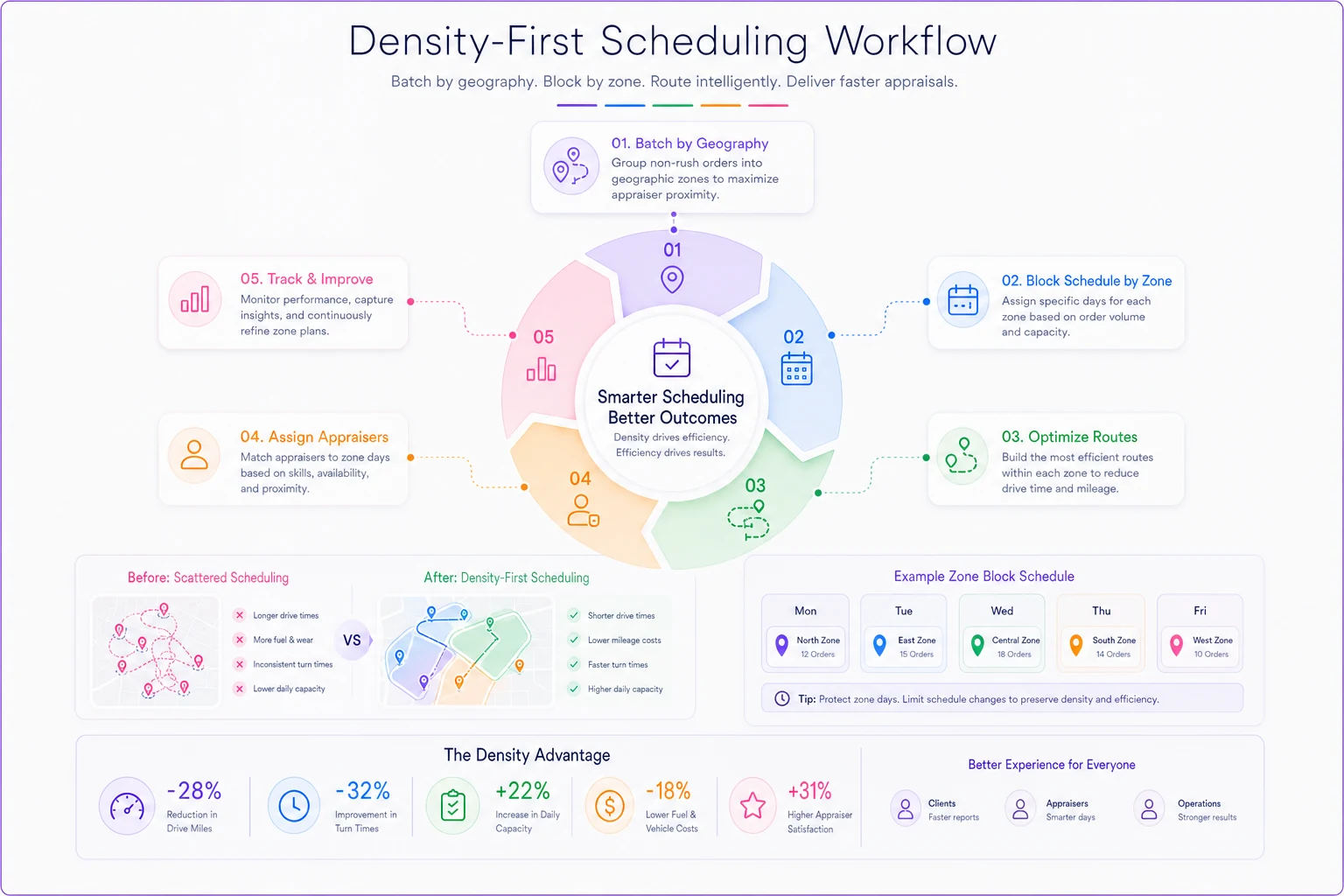

Reschedule for density, not speed

Traditional scheduling prioritizes turn time. Order comes in Monday, assign immediately, complete by Wednesday. That made sense when volume was high and predictable.

Now you need density-first scheduling. Hold non-rush orders for 24-48 hours. Batch assignments by geography. Send appraisers to specific zones on specific days. Yes, this adds a day to some turn times. It also cuts drive miles by 25-30%.

The math isn't complicated. An appraiser hitting four inspections in the same ZIP code spends maybe 90 minutes traveling. The same appraiser covering four scattered properties burns 3.5 hours on the road. That's two hours of lost productivity and around $28 in additional vehicle costs—per day, per appraiser.

This illustrates a density-first scheduling workflow.

Quoting 5-day delivery and hitting it 95% of the time beats promising 3 days and scrambling constantly.

Firms already running optimized routing and block scheduling systems can adjust their zones weekly based on order flow. Manual scheduling shops need at least three weeks to restructure coverage maps—which is exactly why July matters more than September.

The staffing flexibility gap

When refinance volume drops 30% but purchase appraisals only increase 10%, you're looking at net negative 20% order flow. Most firms handle this poorly. They either keep full staff and watch utilization crater to 65%, or they cut too deep and can't handle the rush periods that always come back.

The answer isn't contractors versus employees. It's building real capacity flexibility into how your operation is structured.

Start with your inspection-to-report ratio. Most firms run roughly 1:1—each appraiser handles both field work and report writing for their own properties. Split this. Create inspection-only roles and report-writing-only roles. Now you can scale field capacity without touching report production.

A firm in Phoenix implemented this split model in May. They kept three full-time report writers steady while scaling field inspectors from six down to four. When purchase demand spiked during a two-week June heat break, they brought in two contract inspectors for just those weeks. Report quality stayed consistent. Turn times held. Labor costs tracked revenue within 3%.

Build scenarios, not budgets

Static annual budgets assume predictable conditions. That assumption hasn't been reliable since 2020 and it's not coming back.

-

Base case (50% probability) Order volume drops 15% from current run rate. Margins compress around 2 percentage points. You maintain current staffing but implement geographic batching and selective order acceptance. Cash flow stays positive but tight.

-

Downside case (30% probability) Volume drops 35%. Two major lenders reduce orders. You shift two appraisers to contract status, sublease office space, pause discretionary spending. Focus entirely on highest-margin work.

-

Upside surprise (20% probability) Fed cuts rates unexpectedly. Refi volume surges 40% for 8-12 weeks. You activate dormant contractor relationships, extend operating hours, and potentially decline some low-margin rush orders to protect quality.

Each scenario needs specific triggers and action steps. Not vague plans like "reduce costs" but concrete moves: "When weekly order volume drops below 47 for two consecutive weeks, convert Johnson to contractor status and reassign Northern County coverage to Martinez."

Why September decisions happen in July

The firms that struggle in Q4 are making their mistakes right now. They're waiting for clarity. Hoping volume rebounds. Avoiding hard conversations about pricing and staffing.

But September's cash crunch gets determined by July's operational decisions. Skip repricing now and you'll eat two months of margin compression before catching up. Skip route restructuring and you'll burn unnecessary cash through peak summer driving season. Skip staffing flexibility and you'll face painful cuts right before the holidays.

A three-location firm in Tennessee learned this the hard way in 2023. They waited until October to address obvious cost pressures. By then, they'd burned through roughly $47,000 in excess operating costs, lost two senior appraisers to competitors, and watched their largest lender pull 40% of volume due to inconsistent delivery.

The same firm reorganized operations this past May—ahead of the current CPI pressures. They implemented dynamic pricing, zone-based scheduling, and flexible staffing while business was still strong. Their June margins actually improved despite 18% lower volume.

The operational software advantage in volatile markets

Manual scheduling on whiteboards can't optimize routes across 20+ variables. Spreadsheet pricing can't update dynamically based on real cost data. Email-based coordination falls apart when you need daily staffing adjustments.

AI-powered operational software handles that complexity automatically. Route optimization happens in real-time, factoring in traffic patterns, appraiser expertise, and property clustering. Pricing recommendations adjust based on actual cost tracking. Capacity planning shows you exactly when to add or pull back on field resources.

But the real advantage isn't the automation itself—it's how fast you can adjust. Markets are moving week-to-week now, not quarter-to-quarter. Firms running integrated operational platforms can reprice their entire service menu overnight. Restructure territories in an afternoon. Shift between staffing models without losing coordination.

One mid-sized firm tracked their adjustment speed before and after platform implementation. Previously, a major operational change—like switching from individual routes to zone-based scheduling—took 3-4 weeks to plan and execute. With operational software handling scheduling, routing, and communication, the same change took 3 days.

Making the turn before the cliff

The June CPI numbers aren't catastrophic. This isn't 2008. But they signal a shift that rewards operational discipline over market momentum.

The appraisal firms that hold up through the next 18 months won't necessarily be the biggest or the ones with the best lender relationships. They'll be the ones that adjusted operations in July instead of October. Priced based on true costs, not competitive pressure. Built flexibility before they needed it.

Persistent shelter inflation combined with rising operational costs isn't a temporary squeeze—it's a new baseline. The old playbook of absorbing costs and waiting for volume to return doesn't work when both sides of the equation are moving against you simultaneously.

Start with geographic repricing this week. Map your actual costs per zone, including realistic drive times and vehicle expenses. Add 15-20% premiums for areas beyond your efficient coverage zones. Some clients will push back. Losing unprofitable orders is better than subsidizing them.

Next, restructure scheduling around density. Two days for North County, two days for downtown, one day for outlying areas. Hold orders when necessary to batch efficiently. Your appraisers spend less time driving, more time inspecting, and go home less worn out.

Finally, build real flexibility into staffing. This doesn't mean layoffs—it means creating variable capacity through roles, hours, and coverage areas that can expand or contract with demand. The firms that can maintain quality while flexing capacity will pick up market share from those that can't.

The CPI report is just data. How you respond to it determines whether Q4 is a crisis or an opportunity.

Ready to elevate your appraisal operations?

Join 500+ appraisal firms using Rateoly to enhance accuracy, save time, and improve client satisfaction.