Every appraisal firm gets lender exceptions. That's normal. What isn't normal is seeing the same exceptions month after month — missing flood zone notation, inconsistent GLA calculations, comp age cutoff violations. The difference between firms buried in rework and those running clean operations is pretty straightforward: one has a structured way to understand why exceptions happen and fix the actual cause. The other just fixes the report and moves on.

Most firms handle exceptions reactively. Report comes back, appraiser fixes it, moves on. Three weeks later, same exception, different property. The drain compounds fast — appraisers burning 3-4 hours weekly on rework, coordinators juggling revision tracking, client relationships taking hits from delayed closings.

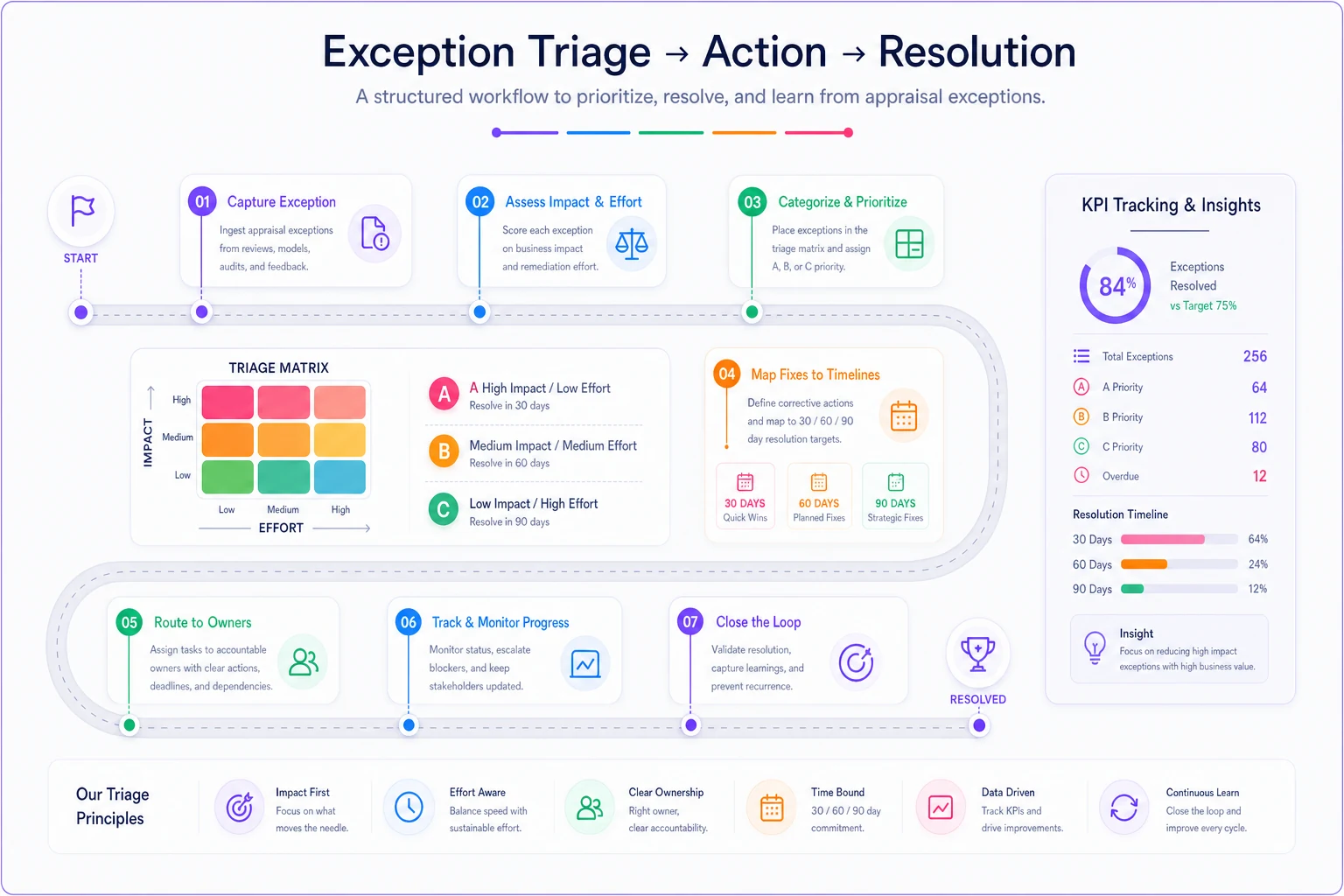

An appraisal exception root cause analysis doesn't need to be some big complicated initiative. The framework here takes about 2 hours to set up initially, then runs mostly on its own with quick weekly check-ins.

Why exceptions keep recurring (hint: it's not appraiser error)

Exceptions tend to cluster around specific patterns. After tracking exception data across multiple appraisal operations, clear categories emerge — and most have nothing to do with individual appraiser mistakes.

Lender requirement drift — Wells Fargo changes their comp age requirement from 6 months to 4 months. Nobody tells the field team. Suddenly you're getting exceptions on reports that would've passed two weeks ago.

Template misalignment — Your standard suburban template works fine for tract homes. Then someone uses it on a rural property with acreage. The template doesn't prompt for required rural-specific narratives. Exception guaranteed.

Data source conflicts — County records show 1,847 sq ft. MLS shows 1,923 sq ft. Tax assessment says 1,880 sq ft. Appraiser picks one without documenting the discrepancy reasoning. Exception comes back asking for reconciliation.

Process handoff gaps — Field inspector takes photos, desk appraiser writes the report. Inspector doesn't capture the converted garage because it looked original from the street. Report goes out stating 2-car garage. Underwriter spots the discrepancy in the photos. Exception.

These aren't training issues. They're systematic gaps that keep generating the same problems until someone actually addresses the underlying workflow.

Building your exception triage matrix

A triage matrix categorizes exceptions by impact and effort to fix. Not all exceptions matter equally. Some delay closings and damage client relationships. Others just create busywork.

Manage every appraisal with confidence and clarity.

Rateoly helps you coordinate inspections, generate reports, and communicate seamlessly with clients.

- Comprehensive appraisal tracking

- Automated client notifications

- Integrated scheduling & report management

No credit card required

Here's the framework:

| Exception Category | Business Impact | Fix Complexity | Priority Score |

|---|---|---|---|

| Comp selection/age | High (delays closing) | Low (rule update) | A |

| GLA discrepancies | High (revision required) | Medium (process change) | A |

| Missing narratives | Medium (quick fix) | Low (template update) | B |

| Photo quality/angle | Low (cosmetic) | Low (training) | C |

| Formatting inconsistencies | Low (aesthetic) | Medium (system config) | C |

Priority scoring:

-

A Priority

Fix immediately, affects revenue or compliance

-

B Priority

Fix within 30 days, affects efficiency

-

C Priority

Fix within 90 days, nice-to-have improvements

This visual shows the triage workflow in simple steps.

The matrix changes how you allocate resources. Instead of treating every exception the same, you focus effort where it actually matters. A comp age violation that delays closings gets immediate attention. A slightly blurry exterior photo gets logged for the next training session.

Sampling rules that catch patterns without drowning in data

Tracking every single exception creates analysis paralysis. You need enough data to spot patterns without overwhelming your operation.

Week 1-2: Track everything. Yes, it's tedious. But two weeks of complete data will show you which exceptions happen constantly versus which are true outliers.

Week 3-4: Switch to percentage sampling based on volume:

-

Under 20 reports/week

Track 100%

-

20-50 reports/week

Track 50% (every other report)

-

50+ reports/week

Track 25% (every fourth report)

Ongoing: Focus tracking on A-priority exceptions only, sample B and C quarterly.

This graduated approach means you're not stuck in data collection mode forever. Once patterns emerge, you lighten the tracking load while still catching new issues.

One firm that went through this process started tracking everything and found roughly 40% of their exceptions came from just three lenders with unique requirements nobody had documented. Two hours updating lender profiles eliminated about half their weekly rework. That's not a complex fix — it's just information that was sitting nowhere useful.

The 30/60/90 remediation roadmap

Fixes need timelines or they never happen. The 30/60/90 framework creates urgency without overwhelming your team.

30-day fixes (Quick wins):

-

Update report templates with missing required fields

-

Add lender-specific requirement flags to order management

-

Create quick reference cards for common exception scenarios

-

Set up a shared exception log visible to all appraisers

Mostly documentation and communication improvements. No new technology, no major process overhauls. Just capturing what you already know and putting it somewhere people can actually find it.

60-day fixes (Process improvements):

-

Implement a pre-submission QC checklist based on top exceptions

-

Standardize data source hierarchy (which source wins when they conflict)

-

Create a lender requirement matrix updated monthly

-

Build a feedback loop from processors back to field appraisers

These require some workflow changes but nothing that disrupts daily operations. The QC checklist alone typically cuts exceptions by 25-30% because it catches issues before submission.

90-day fixes (Systematic upgrades):

-

Integrate automated compliance checking into report workflow

-

Deploy forms software with built-in lender rule validation

-

Establish monthly exception review meetings with action items

-

Create appraiser scorecards showing individual exception rates

The 90-day improvements often involve technology or significant process redesign. They take longer but create lasting operational change rather than just plugging holes.

Tracking KPI impact to prove the ROI

Exception reduction efforts need measurable results or they lose organizational support. These specific metrics are worth tracking:

Primary metrics:

-

Exception rate per appraiser (exceptions/reports submitted)

-

First-time acceptance rate by lender

-

Average revision turnaround time

-

Revenue impact from delayed closings

Secondary metrics:

-

Time spent on rework (hours/week)

-

Client satisfaction scores

-

Repeat exception rate (same issue, multiple occurrences)

-

Staff overtime related to exception handling

A mid-size firm tracking these metrics found their exception rate dropped from 18% to 7% after implementing systematic fixes. Their average revision turnaround went from 48 hours to same-day, which did more for lender relationships than any amount of account management calls.

The tracking doesn't need to be elaborate. A simple spreadsheet updated weekly captures enough data to show trends. Sporadic tracking gives you anecdotes, not patterns.

Real scenario: How one firm cut exceptions by 65%

Regional appraisal firm, 12 appraisers, roughly 180 reports monthly. They were seeing 30-35 exceptions per month, mostly from three national lenders. Each exception took 1-2 hours to resolve — around 50 hours of monthly rework that nobody signed up to do.

Their triage matrix revealed:

-

45% of exceptions

Missing or inadequate market condition commentary

-

30% of exceptions

Comp selection outside lender parameters

-

15% of exceptions

Photo labeling and orientation issues

-

10% of exceptions

Various one-off issues

Their 30-day fix: Updated report templates with required market condition fields and specific prompts. Created a one-page "Big 3 Lender Requirements" guide posted at every workstation.

Their 60-day fix: Built a pre-submission checklist covering the top 10 exception causes. Required a 5-minute peer review before submission using the checklist.

Their 90-day fix: Implemented report management software that flagged missing required fields before submission and automated comp age checking against lender rules.

Results after 90 days:

-

Exception rate

35/month down to 12/month

-

Rework hours

50/month down to 15/month

-

First-time acceptance

81% up to 94%

-

Saved roughly $3,000/month in labor costs

The biggest surprise? Appraiser morale improved. Nothing frustrates professionals more than redoing work because of something that was entirely preventable.

When root cause analysis makes sense (and when it's overkill)

This systematic approach works best for firms handling 50+ reports monthly with recurring exception patterns. If you're seeing the same issues repeatedly across multiple appraisers, you have a system problem worth solving properly.

It's probably overkill if:

-

You handle under 20 reports monthly

-

Exceptions are genuinely random with no patterns

-

You work with a single lender with stable requirements

-

Your exception rate is already under 5%

For smaller operations, a simple exception log with monthly review might be all you need. The full framework becomes valuable when exception management starts eating meaningful operational bandwidth.

Integrating exception tracking with operations

The implementations that actually stick tie exception tracking directly into existing workflows rather than creating a separate process nobody maintains. Your report management system should be capturing exception data automatically. Your regular workflow automation should include exception prevention checks built in.

AI-assisted operational platforms can flag potential exceptions before submission — checking comp dates against lender rules, verifying required photos are present, confirming necessary narratives exist for property type. That kind of pre-submission catching stops most exceptions before they ever leave the office.

The exception data also feeds back into training and process improvement in a useful way. When you know exactly which issues recur, you can target training specifically rather than sending out generic "be more careful" messaging that never actually changes behavior.

Making the system stick

The biggest failure point for exception reduction programs is that they start strong and fade as daily urgencies take over. Three things that help:

Visible scoreboard: Post weekly exception rates somewhere everyone sees them. Not to shame anyone, but to keep awareness up. When numbers are visible, they get attention.

Quick wins first: Start with the easiest, highest-impact fixes. Early success builds the buy-in needed for bigger changes down the line.

Regular reviews: Schedule 15-minute weekly exception reviews. Same time, same day. Review new patterns, assign fixes, track progress. Keep it short and don't let it turn into a meeting about meetings.

Start with visible team-level weekly rates rather than individual names to encourage improvement without shaming.

Firms that succeed with this treat exception reduction like any other critical business metric — consistent tracking, regular review, clear accountability for improvements.

The compound effect of systematic fixes

Each exception you prevent saves more than just revision time. It preserves client confidence, reduces appraiser frustration, prevents revenue delays, and frees up capacity for actual growth.

A 10% reduction in exceptions might save 20 hours monthly. The real value is what you do with those 20 hours — more volume, better processes, or just less daily firefighting that grinds people down.

The framework here — triage matrix, smart sampling, phased remediation, KPI tracking — turns exception management from reactive scrambling into something you actually control. You stop treating symptoms and start preventing problems.

Start simple. Track exceptions for two weeks. Build your triage matrix. Fix the top three issues. The compound benefits build faster than you'd expect once you stop accepting recurring exceptions as just part of the job.

Ready to elevate your appraisal operations?

Join 500+ appraisal firms using Rateoly to enhance accuracy, save time, and improve client satisfaction.